SDG 7: Progress and Barriers to the 2030 Commitment

Background

In 2015, the Sustainable Development Goals (SDGs) were adopted by the 193 Member States of the United Nations at the 70th session of the United Nations General Assembly (UNGA), setting 17 global goals and 169 targets to be achieved by 2030. SDG 7 specifically aims to "ensure access to affordable, reliable, sustainable and modern energy for all," recognizing that energy is fundamental to poverty reduction, economic growth, health, education, and climate action. As of 2026, only about 36% of measurable SDG targets are on track or making moderate progress, about half are making marginal progress, and about 15% have regressed below their 2015 baseline. While SDG 7 has seen gains in renewable energy deployment and electricity access, progress remains too slow to meet the goal of universal access by 2030, as set out in the 2030 Agenda for Sustainable Development adopted at the UN Sustainable Development Summit in September 2015. With four years remaining, substantial acceleration in implementation and investment will be necessary to sustain biodiversity and economic growth and to strengthen mitigation and adaptation capacities for managing climate change.

Target 7.1: Access to Electricity

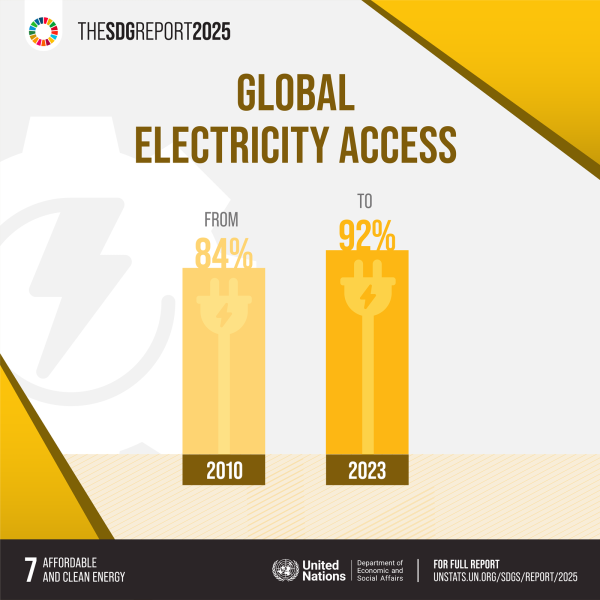

Since 2015, access to electricity has reached 92 percent of the global population. From 2023 to 2024, renewable energy capacity per capita also grew by 14 percent, and internet usage reached 74 percent of the global population in 2025. Access to clean cooking also rose by 11 percentage points to 75% since 2023. Additionally, charcoal, coal, and animal waste are still relied on for cooking. Despite the USD 36 billion investment for electricity access in 2017, only a third of this was estimated to support new vulnerable communities. Progress has stalled in many hard-to-reach areas of the world, with about 655 million people still without access to electricity in 2024, largely concentrated in Sub-Saharan Africa. Finance commitments in Sub-Saharan Africa remain extremely low, as only 4 of 12 African HICs reported a decline in electricity investment. Further investments in fossil fuel plants intensify reliance on centralized grids as coal plants and wires for rural villages become costly. The COVID-19 pandemic also triggered a spike that erased years of progress.

Source: United Nations Sustainable Development Goals, Affordable and Clean Energy infographic.

Currently, 20 nations in Sub-Saharan Africa and Asia have the most significant gaps in electricity and renewable energy access. To meet the 2030 target, energy efficiency and electrification must at least double. As of 2026, less than a fifth of African countries have targets to reach universal electricity access by 2030. Further efforts are also necessary in Afghanistan, Mongolia, and Pakistan. An average investment of at least USD 50 million per year will be required to ensure universal access to electricity by 2030; this is the minimum to afford power generation and electricity networks. It’s also worth exploring mini-grids and off-grid systems to bring electricity to remote areas.

Over 2 billion people lack access to clean cooking facilities, utilizing solid biomass, charcoal, kerosene, coal, and animal waste as their primary sources of fuel. Household air pollution from these fuels remains linked to approximately 2.9 million premature deaths each year, with women and children facing the greatest health risks due to longer exposure to indoor smoke. Progress has been especially slow in Sub-Saharan Africa, where population growth continues to outpace gains in access to clean cooking. As a result, the number of people without access in the region has continued to increase despite improvements in overall access rates.

Financing remains one of the biggest challenges to accelerating progress. Clean cooking receives only a small share of international energy access finance compared to electricity access, limiting the deployment of cleaner fuels and technologies. Affordability also remains a challenge, as many households cannot afford the upfront costs of clean stoves or reliable fuel supplies, even when they are available. Weak infrastructure, limited fuel distribution networks, and inconsistent national policies have further slowed implementation, particularly in rural and vulnerable settings.

Despite these challenges, universal access to clean cooking by 2030 remains achievable. The International Energy Agency estimates that around $8 billion in annual investment would be sufficient to provide universal access to clean cooking by 2030, a small share compared to global energy investment. Scaling concessional finance, targeted subsidies for low-income households, and public-private partnerships can also potentially lower costs and expand adoption. Possible solutions should also be tailored to the local context, including electric cooking where reliable electricity is available. Additionally, expanding access to clean cooking would not only improve health outcomes but also reduce pressure on forests, lower greenhouse gas emissions, and free up time for women and girls to pursue education and economic opportunities. Since the COVID-19 pandemic, progress has been further delayed by reduced incomes and higher prices for clean cooking fuel.

Target 7.2: Renewable Energy

Renewable energy continues to make steady progress, reaching 18% of total final energy consumption in 2023, up from 15.6% in 2015, while the share of modern renewables increased from 10.2% to 13.4% over the same period. As of 2026, renewables make up over 30% of global electricity generation, mainly due to rapid growth in solar and wind power; this overtakes coal consumption. Even so, progress remains uneven across sectors; renewable energy accounts for only 21% of heating and 4.3% of transport, as reliance on fossil fuels continues to slow the energy transition.

Although renewable energy deployment reached record levels in recent years, the pace of growth remains insufficient to meet the 2030 target. Grid infrastructure, energy storage capacity, and transmission networks have especially struggled to keep pace with new renewable generation, delaying the integration of additional clean energy into electricity systems. Investment also remains uneven, with much of global renewable finance concentrated in advanced economies and a handful of emerging markets, while many developing countries continue to face high borrowing costs and limited access to capital. Lengthy permitting processes, supply chain disruptions, and growing demand for critical minerals have also created bottlenecks for expanding renewable energy projects.

Accelerating progress will require higher investment in renewable generation, modernizing electricity grids, and expanding energy storage. Greater international cooperation and policies that lower investment risks can help mobilize private capital, particularly in developing economies where renewable energy potential remains largely untapped. Expanding renewable energy across the heating and transport sectors through electrification, sustainable fuels, and cleaner technologies will also be important to keeping SDG 7 within reach.

Target 7.3: Energy Efficiency

Global primary energy intensity improved by 1.5% in 2023, down from 2.4% in 2022, but slightly above the average annual improvement of 1.4% between 2015 and 2023. While several major economies outperformed the global average, the current pace remains below the 2.6% annual improvement needed between 2015 and 2030 to achieve SDG 7. Without significant acceleration, it’s very unlikely for the world to meet its energy efficiency target by the end of the decade.

Several factors continue to slow progress. Rising global energy demand, aging infrastructure, and even continued reliance on energy-intensive industries have offset efficiency gains in many countries. Although more efficient technologies are becoming available, their adoption remains constrained (especially in developed countries) due to high upfront costs, limited financing, and weak policy implementation. Developing countries also face additional challenges in upgrading buildings, industrial facilities, and transportation systems because of limited technical and financial capacity.

Accelerating energy efficiency remains one of the most cost-effective ways to reduce emissions, lower energy costs, and strengthen energy security. Accelerating investment in energy-efficient buildings and industrial processes, alongside stronger building codes and minimum energy performance standards, will help countries reduce energy demand without compromising economic growth. Greater international cooperation, technology transfer, and financial support will also be essential to help developing countries deploy energy-efficient technologies at scale.

SDG 7 remains a global commitment, but achieving universal access by 2030 will be out of reach without aggressive actions. Infrastructure constraints, limited investment, and growing energy demand will all continue to slow implementation, especially in developing countries; this raises questions as to how realistic this commitment is from an implementation standpoint due to a lack of benchmarks, pre-existing coordination challenges, and infrastructural limitations. Many of the solutions, however, are already known. Strengthening international cooperation, expanding renewable energy systems, increasing investment in energy efficiency, and supporting clean cooking initiatives can all help accelerate progress long-term. In Africa, a handful of countries are heading towards a greener future; in South Africa, major solar and wind investments were aggressively implemented through the Renewable Energy Independent Power Producer Procurement Programme (REIPPPP) and rising private sector corporate power agreements. This includes the 100 MW Redstone Concentrated Solar Power plant. In Morocco, we’re seeing the Noor Midelt (800 MW) and Tarfaya (301 MW) Wind Farms. Kenya shows similar progress through geothermal powerhouses and green hydrogen via Tsau Khaeb in Namibia. Central and Southern Asia also shows promising results, having slashed electricity shortages from 414 million to just 27 million by 2023. Internationally, various agreements are pushing renewable energy deployments, including the 2025 Dar es Salaam Declaration.

Improving affordability, reliability, and sustainability will not only advance SDG 7 but also strengthen progress toward poverty reduction, economic growth, health, education, and climate action under the 2030 Agenda. Fundamentally, we would need to change how energy is produced, distributed, and consumed. Greater investment, ongoing innovation to address socioeconomic challenges, and long-term collaboration among the private sector, NGOs, governments, and civil society will accelerate the pace. Access to energy is a fundamental global challenge; education, health care, and economic development are restricted without reliable energy. As climate change continues to affect marginalized communities disproportionately, the shift to clean energy is paramount for protecting wildlife and maintaining a sustainable future.

EDITOR’S NOTE: TBG provides global solutions focused on Sustainability, Innovation and Impact. We leverage a Global Network comprised of more than 1000 experts in over 150 countries. Through TBG Consulting, TBG Global Advisors, TBG Purpose and TBG Capital, we undertake a wide range of projects — from Kenya to Kazakhstan — and transform challenges into opportunities.